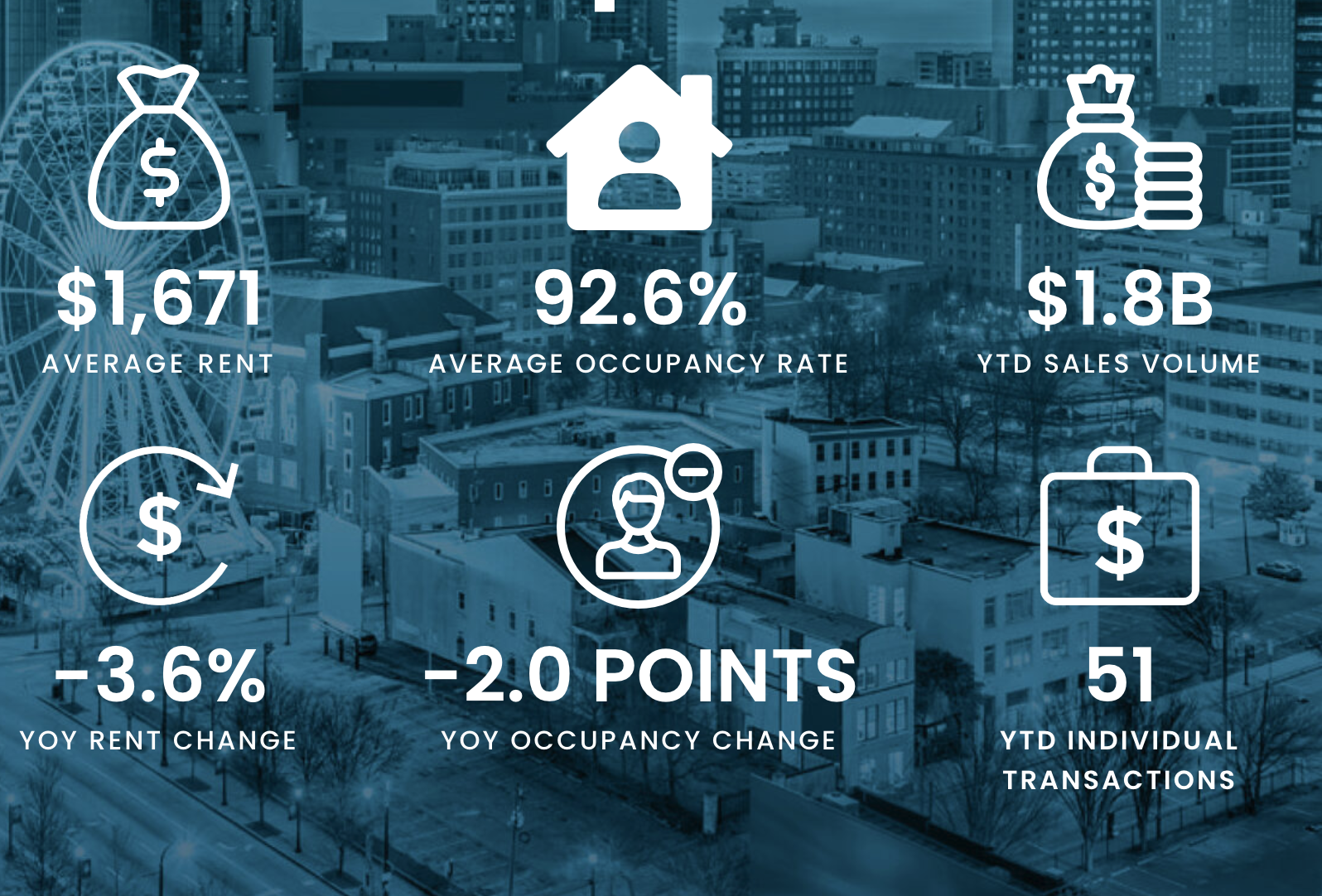

Atlanta continued to see strong in-migration in 2022 and 2023. According to data from the Bureau of Labor Statistics, the Atlanta metro area gained roughly 141,000 new residents through in-migration. Job growth and job diversity continue to be strong across the entire area. Atlanta has always had strong median household income and this was pushed towards $83,000 per year in 2023. According to the Atlanta Association of Realtors, the Average Monthly Mortgage payment for the MSA is $2,851, which is well below the Average Monthly Rent of $1,671.

While these are solid tailwinds for the Atlanta market, there are some headwinds that investors will have to contend with stretching into early 2027. Currently, Atlanta has 42,000 new units scheduled for delivery and this glut of new supply will likely contribute to higher vacancy rates. This will be especially true for the Class B and Class C segments of the multifamily market. On the other hand, the renter pool does remain strong and net absorption should still be a net positive. I predict vacancy to hover around 7.5 to 8.5 percent for the next 24 months. Another side effect of this new supply is suppression of rent growth rates. Atlanta saw explosive rent growth during the pandemic but effective rent growth likely will be less than national averages over the next year.

According to Matthews Real Estate Investment Services, Gwinnett County and North Gwinnett are some of the hotbeds for new construction activity. Gwinnett boasts ample land, a friendly development environment and ample job opportunities across many different sectors. However, across the MSA, particularly in the suburbs, there is a growing aversion to new multifamily development which has stymied development. Many counties and cities have slowed approval of new apartment projects and in some cases placed moratorium on new multifamily development.

Atlanta did experience a significant decrease in the number of units trading hands in 2023 The difficult lending environment and compressed cap rates have pushed many investors to the side for the foreseeable future. The average sale price for assets in northern and northwest submarkets traded for around $219,000 per unit while submarkets located south and west of the city traded coming in at a lower price per unit cost. Some notable submarkets that are often under the radar are Newnan, Fayetteville, Peachtree City and McDonough. These southern suburban communities have solid household formation, strong median income and top ranked schools making them an attractive destination for tenants. Market Outlook

Despite slowing rent growth and supply surge coming to market, the Atlanta MSA is still poised to perform well in the coming years. Renter demand remains strong and the expanding renter pool of 20 to 34-year potential tenants should contribute to strong occupancy and overall market resilience.